INFLATION CALCULATION

The data are currently published in 2010 base.

Since 1986, five bases have followed one another: base 80, base 95, bases 2000, 2005 and 2010.

In other words, when a base shows too much rise in the indices, the ECB changes its base and even changes the composition of the basket which is supposed to be BASE = 100

Let’s take an example: if the BASE 1980 = 150 in 1994:

- The ECB resets the counters to 100 in 1995, then in 2000, then in 2005 and then in 2010;

- In the meantime, the ECB adds, removes or minimizes “troublesome” consumption items such as: property prices, rents, energy, tobacco, taxes, taxes and fees, antiques and works of art, etc.

- It gives too much weight to manufactured products that regularly change volume (downsizing), ingredients (unnecessary supplements, additives of all kinds) and even the percentage of raw materials (water in frozen products), etc.

And so, official inflation rarely exceeds the “2% annual target”.

Indeed, all you have to do is change the base and the basket, and no one will be able to reconstruct the real inflation rates.

In addition, official inflation rates are “harmonised” according to the weight of national economies.

However, EUROSTAT publishes several indices by sector (foodstuffs, housing prices, civil servants’ salaries, etc.) and by country, which show that, even if we take bases higher than 2014 (BASE 2015 = 100), the price indices are far from being comparable and convergent:

- Foodstuffs: the indices for April 2026 are therefore officially very low everywhere in Europe (between 101 and 102) except in the countries where food is the healthiest (Portugal, Romania) and other non-euro countries (Iceland, Kosovo);

- Housing: in 2025, the indices by country could vary from 116 (Italy) to 249 (Bulgaria) or even to 221 (Ireland), 258 (Lithuania) and 165 (Luxembourg) against 127 (France), 153 (Germany) and 145 (Belgium).

Clearly, these indices are calculated on behalf of the ECB and the European Union.

They “forget” that one of the main functions of a currency is its Reserve Function and its Functions of Credit and Capital.

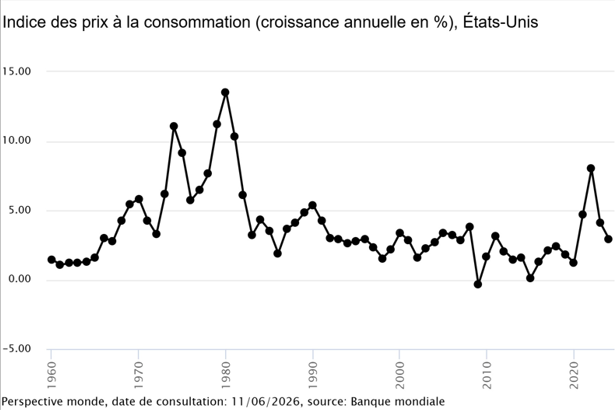

INFLATION HAS PICKED UP SINCE 2020 AND ESPECIALLY SINCE 2026

This resumption of inflation is unofficial since it is energy and raw materials that have exploded, and these items are not properly integrated into the official indices.

The proof?

Official inflation is almost stable.

THE DISASTER OF THIS INTEREST RATE POLICY.

To fight inflation, the worst policy is precisely to kill investments and companies because, in the absence of domestic production, this policy leads to massive imports from countries whose industrial investments are underused, due to a lack of domestic demand.

This is the case in China, where citizens refuse to buy because they cannot afford it or simply because they prefer to save to meet their future pension minimum and face the bad days to come.

Indeed, in China, Africa and many other countries, parents can no longer count on the support of their children to meet their minimalist needs as soon as illness and old age require retirement.

They have fewer children, and they are increasingly impoverished by financial speculation.

So they consume as little as possible.

They save.

THIS POLICY HAS KILLED AMERICA

Paul Volcker, Undersecretary of the Treasury (1963-1965) and then Chairman of the Federal Reserve Bank (1979-1987), raised interest rates from 11.2% to 20% (1979 – 1981) and was the father of a memorable recession.

And yet, the media and economists consider to be “the big winner of stagflation”, real growth (constant prices) supposedly equal to zero.

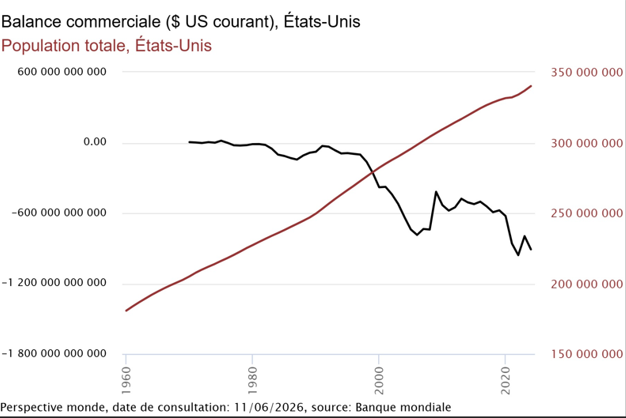

In reality, it has killed the entire wonderful industrial fabric of the United States (excluding armaments) to the point that the balance of goods has become more and more in deficit despite a near doubling of its population (from 180 million in 1960 to 340 million in 2024).

By “giving” jobs and decent wages to a growing population, the United States should have increased its domestic investment in agriculture, consumer goods, and industrial goods.

Instead, U.S. governments have allowed their companies and large distributors (food and household capital goods) to relocate their production to low-wage countries.

Today, they are in unfair competition with their former subcontractors.

It should be noted that all the G7 countries have copied and accelerated this process since the early 1980s.

The result?

Here it is.

THE MECHANISM OF THE DISAPPEARANCE OF OUR CENTRES OF CIVILISATION

As imports into the G7 countries increase, the economic and financial situation in these countries deteriorates.

This regression of the G7 countries is real: it is enough to deduct the National Debt Deltas from the National Production Deltas: ∑ (Δ GNP – Δ PUBLIC DEBT) over thirty years (1995 – 2025).

We are neither in “stagflation” nor in “recession” but in a more worrying phase of the Disappearance of our Centers of Western and Japanese Civilization.

Compared to the G7 countries, the countries under military dictatorship supporting an expansionist policy do not offer a more serene future: certainly, the weapons they produce create GNP, but they are destined to be destroyed in open and latent wars.

In addition, in this field, obsolescence is very rapid in the face of new weapons and tactics.

This mechanism therefore destroys jobs, incomes and lives without creating useful and lasting tangible assets.

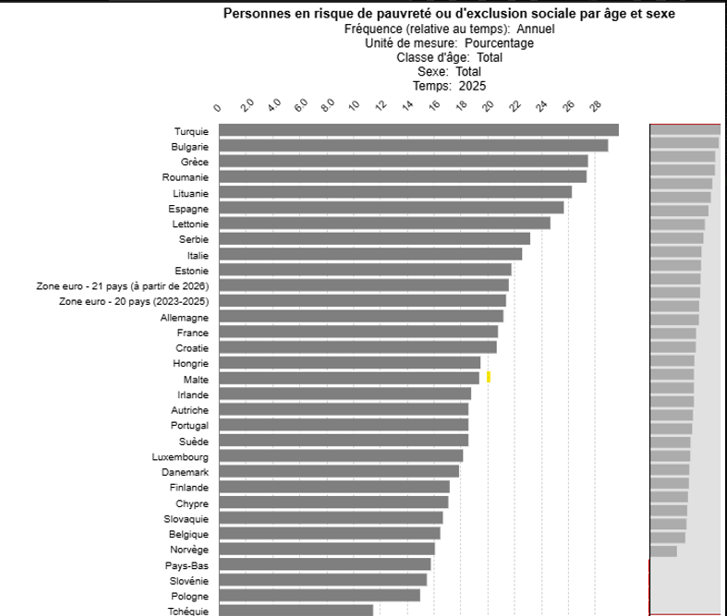

EUROSTAT closely monitors the evolution of poverty by the at-risk-of-poverty rate:

“The at-risk-of-poverty rate is defined as the share of persons with an equivalised disposable income (after social transfers) below the at-risk-of-poverty threshold, set at 60% of the national median equivalised disposable income after social transfers.

It is not an indicator of wealth or poverty.

It merely offers a point of comparison of low incomes with the incomes of other inhabitants of a given country.

However, such an income does not necessarily imply a lower standard of living.”

In other words: more and more residents risk not even having an income of 60% of the median disposable income (50%) despite social transfers:

- 16.3% in the EU-27

- 16.9% in the Eurozone (21 countries)

- 10.9% in Belgium

- 19.5% in Spain

- 22.6% in Lithuania

- 14.8% in Luxembourg

- 16.3% in France

- 16.1% in Germany

CONCLUSIONS: WHY THESE “STOP AND GO” POLICIES?

Regularly, central banks in all countries claim to apply key interest rate policies, sometimes lax (low rates), sometimes “repressive” (high rates).

We have just proven that these policies are suicidal, to the point of threatening the great values of our Humanist Philosophy, based on the Hellenistic values of the Cult of Diversity (much more positive than Respect for Diversity.

In other words, our Societies (G7) no longer even respect the essential rights of all citizens, without any exception: the Right to Subsistence (to live with dignity) and the Right to Existence (the will to progress).

And yet, they apply these “suicidal policies”: why.

Clearly, this “suicidal policy” responds to conflicts of interest between the largest economic and financial players:

- The Top-20 commercial bankers defend a policy of high key rates on the condition that they can discreetly refinance themselves at preferential rates with their national central banks.

- The Top-5 insurers defend these same policies of high key rates because they invest more than two-thirds of their medium- and long-term inflows (pension funds, investment funds) in government bonds.

- Multinationals defend high-interest rate policies to avoid any competition with domestic producers on the condition that they can discreetly refinance themselves at preferential rates with Top-20 commercial banks.

Of course, these interests can themselves be contradictory:

- The alliance between the Top-5 insurers and the multinationals has become obvious for reasonable rates because it is the insurers who choose the Top-Managers of these large companies, public and private, national and international. They therefore rely heavily on lavish dividend policies thanks to their “straw men”.

- Large-scale distribution, on the other hand, finances itself on the backs of producers and defends them because they are slaves who can be exploited at will, while uncontrolled imports make it possible to better “control” their purchase prices and especially their margins (apparent and hidden).

Et tous ces conflits d’intérêt concentrent leurs revendications au détriment des peuples.

- Les grandes victimes du système de « la mondialisation heureuse » et de la « financiarisation (indispensable) de l’économie » sont bien sûr les artisans et les entreprises typiquement nationales : TPE, TPI, PME, PMI, ETE, ETI…

- En conséquence, tout le système actuel est appliqué avec une froideur et une rigidité effrayante pour « arbitrer » les intérêts de ce « beau monde » au point que, désomais, la Commission négocie et signe de plus en plus de traités « en toute discrétion » en se passant du vote du Parlement Européen.

“Freedom for a few” has been “written” in the marble of European treaties: a bit like “The Table of Moses”.

In Europe, and especially in the heart of Europe (the Eurozone), it is High Finance that has “written” all the treaties to impose its powers within the European Council and the Commission (its executive body) to the point that the European Parliament is really only “authorized” to vote on implementing decrees.

We must therefore review the Maastricht Treaties and all the other treaties as soon as possible, because the management of our currencies and of “our Europe” is calamitous.

.